Partnership for Financial Equity and Woodstock Institute Release Mortgage Lending Matters

June 29, 2023

Number of Mortgages to Black and Latino/a Households Remain at All-Time Highs for Second Consecutive Year; Boston Losing Buyers of Color with Gateway Cities Gaining

Boston, MA – More Black and Latino/a homebuyers in Massachusetts received home- purchase mortgages in 2021, surpassing the previous high from a year earlier, than at any time in the last thirty years, according to a report released today by the Partnership for Financial Equity. Check out some of the coverage of the report in The Boston Globe and WCVB-5 and WBUR.

Mortgage Lending Matters and corresponding Fact Book was prepared by the Chicago-based Woodstock Institute as part of a multi-year research partnership between the two organizations. These reports represent one of the most comprehensive looks at mortgage lending in Massachusetts with an emphasis on lending to low- and moderate-income households and person of color. Some of the key information and findings in these materials include the following:

•A total of 4,920 Black households and 8,694 Latino/a households obtained home purchase loans in 2021, both of which represent record highs. Total mortgage loan volume also peaked with 81,401 home-purchase mortgages in Massachusetts in 2021.

•Both Black and Latino/a purchasers are receiving roughly the same percentage of first lien, one- to four-family purchase mortgages for owner-occupancy (traditional purchase mortgages) in the Commonwealth as their respective shares of the Commonwealth’s population. Asian buyers receive almost twice the percentage of traditional purchase mortgages as their share of the population, and White buyers slightly less.

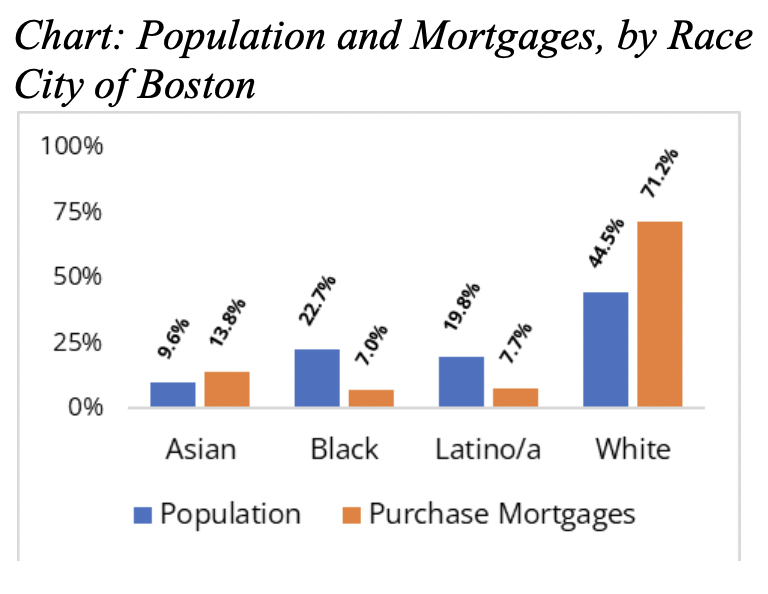

•In Boston, however, Black and Latino/a purchasers are far below their respective shares of the population. For example, Black borrowers receive just 7% of home purchase mortgages in the City of Boston but comprise 22.7% of the population. Latino/a borrowers received 7.7% of home purchase mortgages while comprising nearly 20% of the city’s population. In contrast, White borrowers represent 44.5% of Boston’s population but received 71.2% of the home purchase mortgages in 2021.

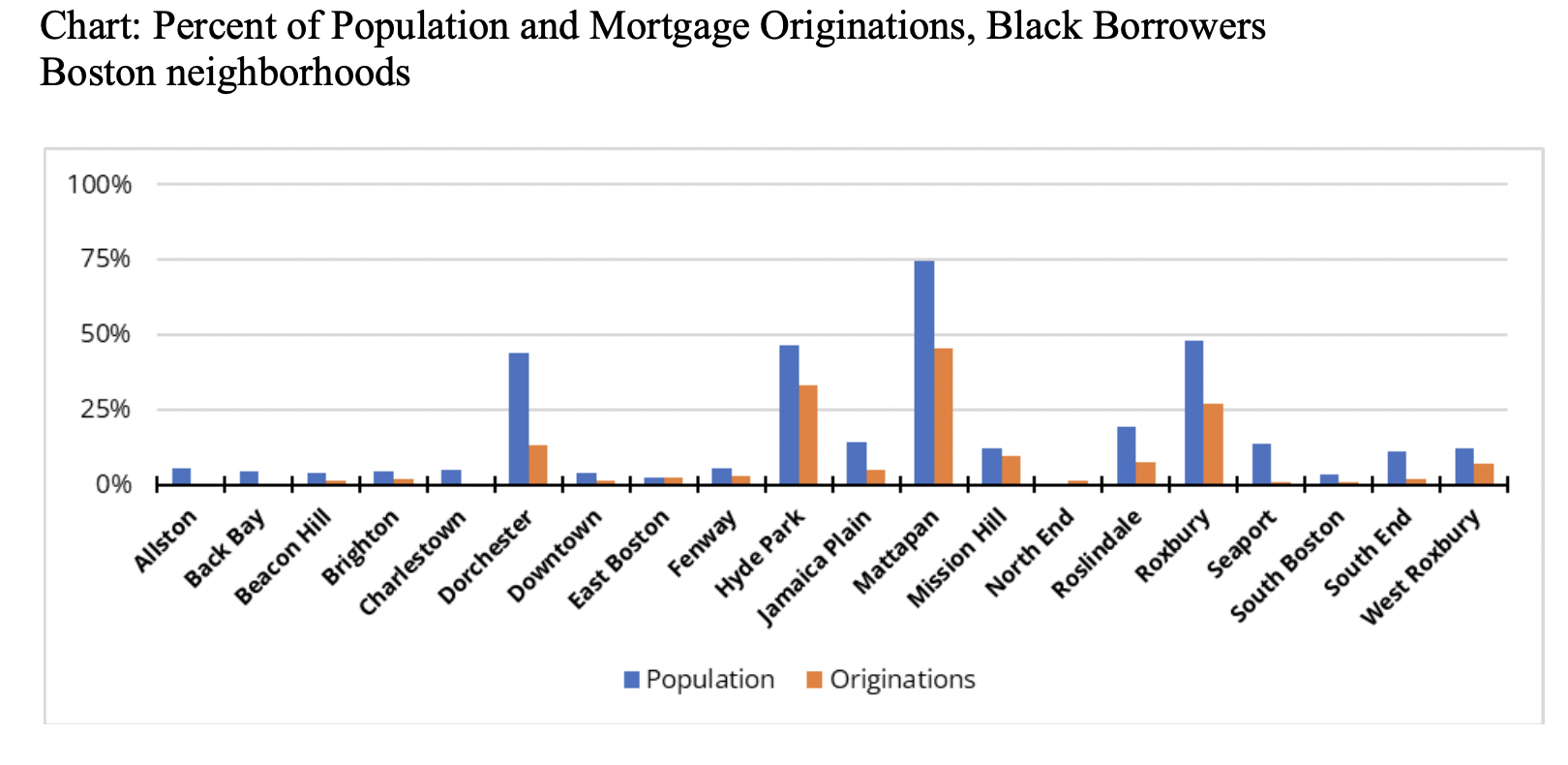

•By comparison Black purchasers in Boston were a smaller percentage of buyers than their existing percentage of the neighborhood population in almost all Boston neighborhoods, especially in Dorchester, Mattapan, Hyde Park and Roxbury. Only in Mattapan, where Black residents are nearly 75 percent of the population, did Black borrowers receive more than a third of traditional purchase mortgages. In two neighborhoods, Allston and Back Bay, no Black borrowers received traditional purchase mortgages, and in three others – Charlestown, Seaport, and South Boston – they received less than one percent of mortgages.

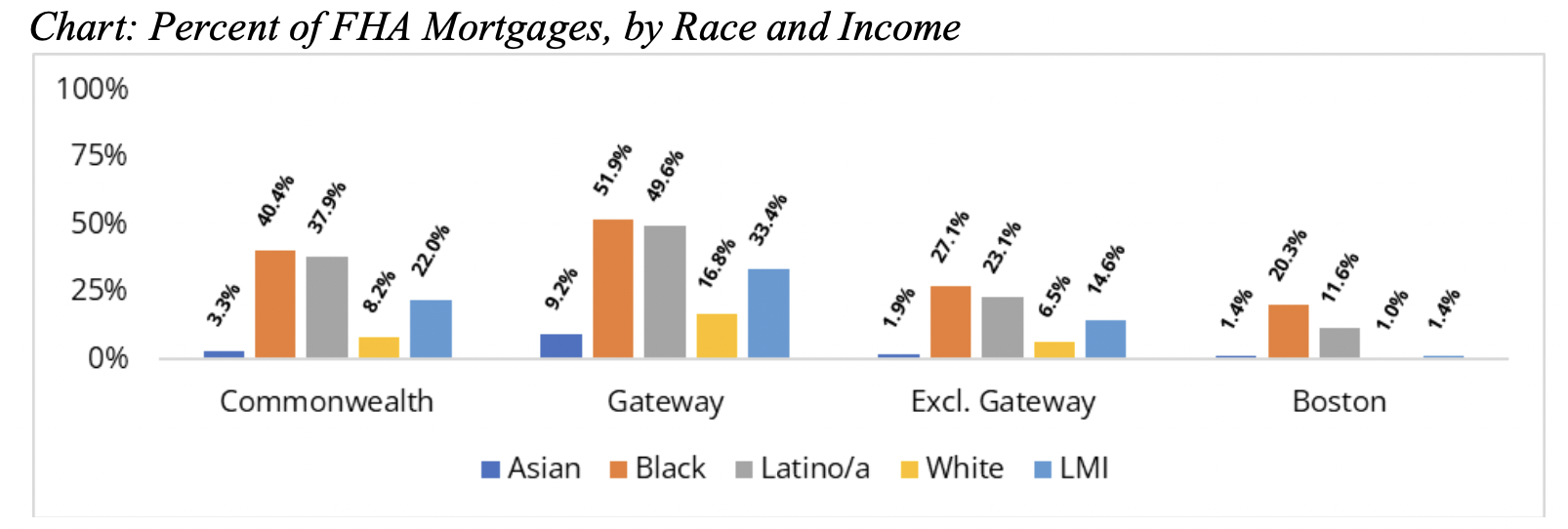

•For traditional home purchase mortgages outside of Boston, Black and Latino/a borrowers are between three and five times as likely as White borrowers, and one and half to two times as likely as LMI borrowers, to have an FHA mortgage. In Boston, Black and Latino/a borrowers are 11 to 20 times as likely as White borrowers, and eight to 15 times as likely as LMI borrowers, to have an FHA mortgage. LMI borrowers are two to three times as likely outside of Boston, and 1.4 times as likely in Boston, to have an FHA mortgage as White borrowers.

•The disparity between Black and Latino/a borrowers and White or LMI borrowers in the percentage of FHA mortgages is also apparent in the percentage of loans with LTVs over 90 percent. Black and Latino/a borrowers had a higher percentage of loans with an LTV over 90 than White, Asian or LMI borrowers. Over 80 percent of all Black and Latino/a borrowers receiving tradtional mortgages in Gateway Cities had LTVs over 90 percent, meaning that they made down payments of less than 10 percent of the purchase price.

Most Active Lenders

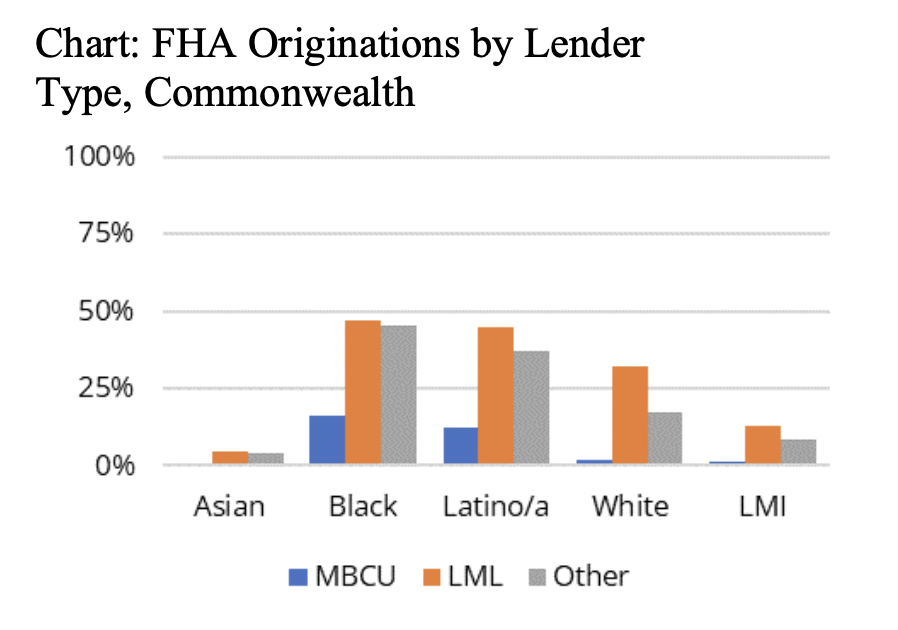

•Overall, Licensed Mortgage Lenders (LMLs) originated 51 percent of all purchase and refinance mortgages combined in the Commonwealth, 58 percent in Gateway Cities, 49 percent outside of Gateway Cities, and 47 percent in Boston. Massachusetts Banks and Credit Unions (MBCUs) originated 34 percent of all mortgaes in the Commonwealth, 27 percent in Gateway Cities, 36 percent outside of Gateway Cities, and 40 percent in Boston. Of the top ten mortgage originators, eight were LMLs in the Commonwealth and outside of Gateway Cities. Nine out of the top ten were LMLs in Gateway Cities, but just six out of the top ten were LMLs in Boston.

•LMLs originated 51 percent of purchase mortgages in the Commonwealth, with higher percentages of originations for some groups. They originated 54 percent of all purchase mortgages to Black borrowers, 56 percent for Latine borrowers, and 48 percent of purchase mortgages to LMI borrowers statewide. They originated even higher percentages of purchase mortgages for each of those groups in Gateway Cities, 58 percent for Black borrowers, 60 percent for Latine borrowers, and 52 percent for LMI borrowers. Outside of Gateway Cities, MBCUs had a larger share of purchase originations than in either the Commonwealth as a whole of Gateway Cities, although they still originated a smaller percentage of purchase mortgages for Black, Latine, and LMI borrowers than LMLs did. In Boston, MBCUs originated nearly as many mortgages for Black, Latine, and LMI borrowers as LMLs.

Ultimately, Mortgage Lending Matters comes with recommendations to continue the pursuit of home ownership equity in Massachusetts. While more Black and Latino homebuyers have been reached in the home purchase market than ever before, the report calls for steps to maintain that progress including enforcement of fair housing, fair lending and community reinvestment laws. The report recommends greater investment of public dollars for more affordable homeownership opportunities throughout the Commonwealth, more fair lending testing, greater diversity in hiring, and more focus on narrowing the racial homeownership gap from everyone involved in the homeownership process, including real estate agents, lenders, insurers, appraisers, public officials and everyone involved in turning a renter into a homeowner.

About the Partnership for Financial Equity

The Partnership for Financial Equity was established in 1990 to bring together community organizations and financial institutions to affect positive change in the availability of credit and financial services across the Commonwealth by encouraging community investment in low- and moderate-income communities and communities of color. We are funded through the financial support of member financial institutions, community development organizations and others. Our Board of Directors consists of an equal number of representatives from leading community organizations and financial institutions.