Annual Mortgage Lending Matters Report Released

July 24, 2024

Number of Mortgages to Black and Latine Households Remain at Proportional Shares Despite Rising Interest Rate Environment; Racial Gaps in Denial Rates Remain Large, Unyielding

Boston, MA – While the total number of home purchase mortgage loans dipped considerably in 2022, Black and Latine homebuyers in Massachusetts received home purchase mortgages that roughly equaled their relative population share, reaching this mark for the third year in a row, according to a report released today by the Partnership for Financial Equity and the Woodstock Institute.

Mortgage Lending Matters represents one of the most comprehensive looks at mortgage lending in Massachusetts with an emphasis on lending to low- and moderate-income households and persons of color. Some of the key information and findings in these materials include the following:

•It got harder to get a mortgage in 2022. Origination rates plummeted and denial rates rose across all geographies and racial/ethnic groups. Black and Latine applicants continued to be more likely to have lenders deny their applications than either Asian or White applicants but denial rates rose for all racial and ethnic groups. Mortgage applications from white borrowers were denied 13.7% of the time, up from 9.5% in 2021. Black borrowers denial rates were 25% in 2022 up from 18.2% in 2021. Denial rates for Latine borrowers were 23% in 2022, up from 15.4% in 2021. Denial rates for Asian borrowers rose to 14% in 2022, up from 9.4% in 2021.

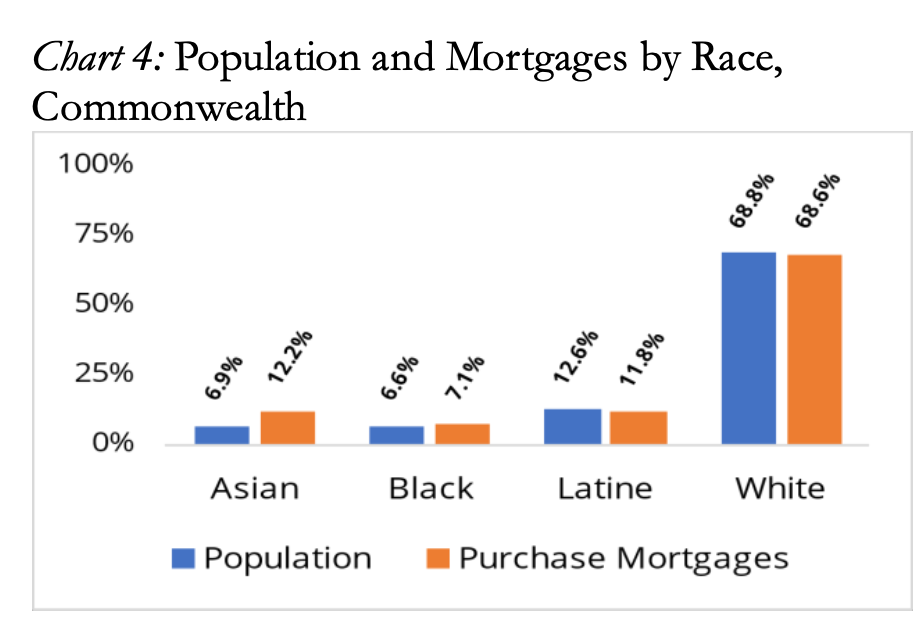

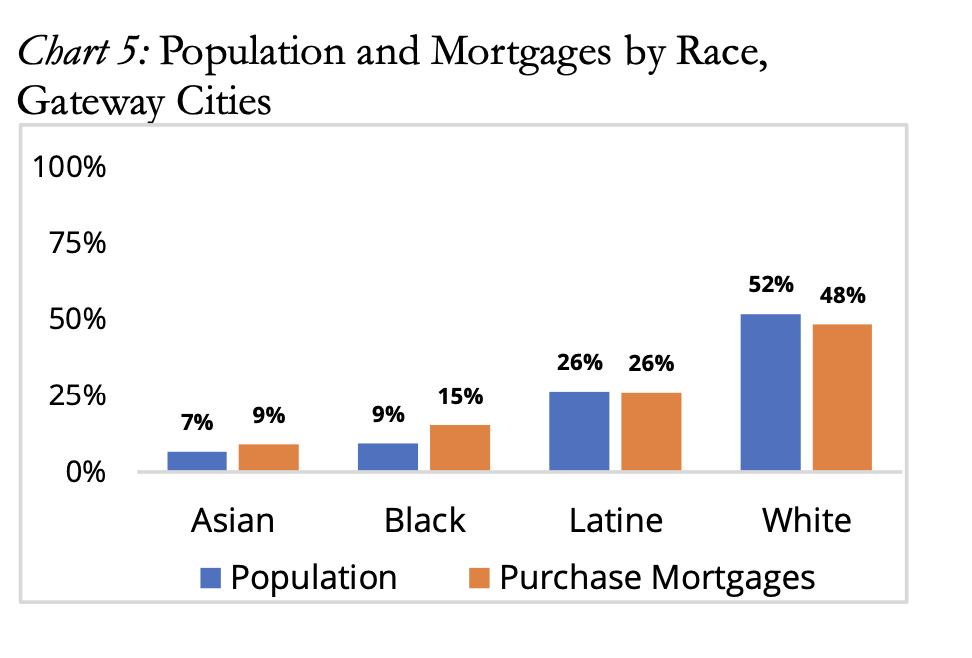

•Black, Latine, and White purchasers received roughly the same percentage of 1st lien, one- to four- family purchase mortgages for owner-occupancy (traditional purchase mortgages) in the Commonwealth as their respective shares of the Commonwealth’s population. Asian buyers received almost twice the percentage of traditional purchase mortgages as their share of the population. In Gateway Cities, which already have higher percentages of Black and Latine residents (close to 36 percent combined) than the Commonwealth as a whole (19 percent), Black and Latine purchasers received a combined 41 percent of traditional purchase mortgages.

•In Gateway Cities, Black and Latine borrowers were roughly three times as likely as White borrowers to have an FHA mortgage, usually a higher cost option compared to mortgages offered by MassHousing and Massachusetts Housing Partnership.

•Over 80 percent of Black and 75 percent of Latine borrowers receiving traditional mortgages in Gateway Cities had Loan-To-Value (LTV) percentages over 90, meaning that they made down payments of less than 10 percent of the purchase price.

•With the exception of Asian borrowers in Boston, 2022 saw increases in the percentage of loans with high debt-to-income ratios for all borrower groups.

•The median loan amount for Black borrowers in the Commonwealth was $425,000 for properties with a median value of $465,000, or an LTV ratio of 91, compared with a median loan amount of $435,000 for properties with a median value of $555,000, for an LTV ratio of 78, for White borrowers

•In 2022 in Boston’s neighborhoods, only Hyde Park, with a Black population of 46 percent, and Mattapan, where over two-thirds of the residents are Black, had over one-third of traditional purchase mortgages go to Black buyers, 48 percent in Mattapan and 38 percent in Hyde Park. In Back Bay, Beacon Hill, and Fenway, no Black Borrowers received traditional mortgages and in Downtown and South Boston they made up less than one percent of the mortgages.

•Only in Hyde Park did Latine borrowers receive more than 20 percent of traditional purchase mortgages (down from 25 percent in 2021). In two other neighborhoods—Mattapan and Roxbury—they received 15 percent of the traditional mortgages. The biggest difference between the percentage of the population and mortgages continued to be in East Boston, where the population was roughly 54 percent Latine, while they only received just over 12 percent of traditional mortgages. In Fenway and Mission Hill, no Latine borrowers received traditional purchase mortgages even though Latines comprise almost 13 percent and 20 percent of the respective neighborhoods.

•Low- to moderate-income borrowers received more than 30 percent of traditional mortgages in five neighborhoods—Brighton, East Boston, Hyde Park, Mattapan, and Roxbury.

•Overall, Licensed Mortgage Lenders (LMLs) originated 38 percent of all purchase and refinance mortgages combined in the Commonwealth (down from 51 percent in 2021), 48 percent in Gateway Cities, 35 percent outside of Gateway Cities, and 30 percent in Boston (down from 47 percent in 2021)

Mortgage Lending Matters concludes “For all the good policy ideas over the past thirty years, we have failed a generation of homebuyers by not building enough housing. Our public investment in housing is lacking given our status as the third- highest cost state in the nation for homeownership (behind just HI and CA). And given this limited pie of housing resources, only a sliver (normally less than 10%) is devoted to affordable homeownership opportunities.”